Introduction

You bill $15,000 in a single month, then forget to follow up on three invoices. You've maxed out a retirement contribution but haven't opened your bank statements in six weeks. You know exactly what you should be doing with money — and you still don't do it.

This is the high-achiever paradox: strong income, real expertise, genuine financial chaos underneath.

The gap isn't a character flaw or a discipline problem. It's a predictable consequence of how the ADHD brain is wired. Generic financial advice fails ADHD professionals for a specific reason: those systems were designed for neurotypical brains with intact executive function running in the background.

This article offers something different: brain-based, professional-specific strategies for building financial systems that actually hold. Not willpower hacks or shame-fueled spreadsheets. Real structures built for how your brain works.

Key Takeaways

- ADHD's financial struggles are neurological, not moral — executive function deficits make planning, impulse control, and follow-through genuinely harder

- Shame and avoidance are the biggest financial obstacles for high-achieving ADHD professionals, and they must come down before any system can stick

- Automation is the most effective single tool for reducing financial friction in an ADHD brain

- Generic financial advice rarely sticks — ADHD-specific strategies are what create lasting change for professionals

Why ADHD Makes Money Management Uniquely Hard for Professionals

The Executive Function Problem

Managing money isn't one task. It's a sustained, multi-step process requiring nearly every executive function skill simultaneously: working memory (to hold balances and deadlines), planning (to project cash flow), impulse control (to defer purchases), sustained attention (to complete tax prep), and self-monitoring (to catch errors before they compound).

ADHD is a disorder of executive function. Research consistently links adult ADHD to poorer financial outcomes — less income, more debt, less savings, and significantly higher rates of impulse buying and exceeding credit card limits (Bangma et al., 2019; Koerts et al., 2021). By age 40, adults with ADHD face default risk over six times higher than the general population.

Running complex financial tasks through an executive function system under constant stress produces exactly these outcomes — predictably, not as a character flaw.

How Symptoms Show Up in Professional Finances

In a professional context, ADHD symptoms manifest in specific, costly ways:

- Forgetting to invoice clients after completing work

- Avoiding financial statements because opening them feels aversive

- Making impulsive business purchases during hyperfocus phases ("this software will change everything")

- Losing hours to context-switching when trying to complete tax preparation

- Missing quarterly estimated tax deadlines because the due date didn't feel real until it passed

How the Dopamine System Shapes Spending

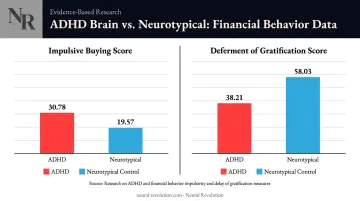

The ADHD brain's reward system heavily favors immediate gratification over delayed rewards — and the research is precise about this. A 2024 study of 225 adults diagnosed with ADHD found impulsive buying scores of 30.78 vs. 19.57 in controls, and deferment-of-gratification scores of 38.21 vs. 58.03 in controls. Long-term financial behaviors — saving, debt repayment, investing — are neurologically difficult for ADHD brains, not lazily avoided.

The High-Achiever Compounding Problem

There's an additional layer for professionals. A salaried employee with a single W-2, employer-sponsored 401(k), and automatic payroll deductions has most of their financial infrastructure handled by default. A consultant, entrepreneur, or self-employed professional has none of that. Variable income, quarterly tax obligations, business expense separation, retirement contributions requiring active decisions — every additional complexity demands more executive function bandwidth.

Each layer of financial complexity compounds the executive function load — and self-employed professionals carry more layers than almost anyone else.

Interest-Based Motivation and Financial Avoidance

Dr. William Dodson's interest-based nervous system model explains why financial tasks so often stall: ADHD brains aren't motivated by importance — they're driven by interest, novelty, challenge, urgency, or passion. A task that lacks those qualities won't get done, regardless of how consequential it is.

Reviewing a bank statement? Low novelty, low urgency (until it's a crisis), zero emotional reward. The ADHD brain isn't ignoring the task — it's genuinely unable to activate for it without the right trigger.

Breaking the Cycle of Financial Avoidance

The Wall of Awful

ADHD educator Brendan Mahan coined the term "Wall of Awful" to describe the emotional barrier that grows from repeated failure — where each avoided task, late fee, or financial mistake adds another layer of shame and guilt that makes the next engagement with money harder. The wall isn't metaphorical. It functions as a real initiation barrier.

For high-achieving professionals, the wall is often taller than average. These are people who expect competence of themselves, who have built careers on discipline and output, and who experience financial chaos as a private humiliation that doesn't match their professional identity. The shame compounds.

The Neuroscience of Avoidance

Adult ADHD research supports a clear link between ADHD, emotional dysregulation, and procrastination. When the ADHD brain associates a task with past stress or failure — an overdue invoice, a tax notice, an unread statement — it generates a threat-adjacent response. Initiating that task feels effortful at a physiological level. This is documented emotional dysregulation, not a motivational character issue.

The practical implication: you cannot solve avoidance purely with a better spreadsheet. The emotional charge has to come down first.

Reducing the Charge Before Building Systems

That means the first move isn't building a better system — it's lowering the emotional charge enough to engage with one. Self-compassion and reframing aren't feel-good extras here; they're practical prerequisites. A system built on top of shame doesn't hold. The moment financial tasks feel like evidence of personal failure, the brain finds ways to delay them.

At Neural Revolution, coaching for ADHD professionals addresses admin avoidance — including financial tasks — as a friction point before building any operational system. The intake process surfaces where avoidance is showing up and why, before recommending structures to address it. That typically includes:

- Identifying which financial tasks carry the heaviest emotional charge

- Running a worth-it threshold analysis to understand why specific tasks aren't crossing the brain's initiation barrier

- Separating practical obstacles (unclear process, missing tools) from emotional ones (shame, past failure)

ADHD-Friendly Budgeting Strategies That Actually Work

Reframe What a Budget Is

A budget isn't a restriction system. It's a map — a picture of what comes in and where it goes. The goal is awareness and decision-making power, not punishment.

For ADHD professionals, the simpler the map, the more likely it gets used. A system you open twice a year isn't a system. A system that takes three minutes to check on a Tuesday morning is.

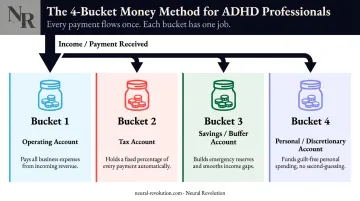

The Buckets Method

The buckets (or jam jar) method separates money into distinct visual categories rather than tracking every transaction in a unified spreadsheet. For ADHD brains, visual separation is more concrete and easier to navigate than abstract totals.

Practical setup for professionals:

- Operating account — regular business expenses and income

- Tax account — a fixed percentage of every payment received, transferred immediately

- Savings/buffer account — emergency reserves and income smoothing

- Personal/discretionary account — what you can actually spend without friction

Each bucket has one job. When the tax account has money, taxes are handled. When the discretionary account runs low, discretionary spending stops. No complex tracking required.

Weekly Money Dates

Monthly financial reviews feel overwhelming for ADHD brains — too much time has passed, too many transactions to reconstruct, too much activation energy to start.

Weekly money dates work better: 10–15 minutes, same time each week, paired with something rewarding (good coffee, a comfortable chair, music). The combination of ritual, predictability, and low time commitment lowers the initiation barrier significantly. The goal isn't a comprehensive audit — it's a brief orientation: what came in, what went out, anything that needs attention this week.

Body Doubling for Financial Tasks

ADHD brains often perform better on tedious tasks when another person is present — even one who isn't actively helping. This is body doubling, and the effect is well-documented.

Options for financial tasks:

- Work alongside a bookkeeper (their presence structures the task)

- Use a virtual co-working session with an accountability partner

- Join a structured virtual body-doubling platform while completing invoicing or expense review

External presence shifts the brain's engagement threshold — no supervision required.

ADHD-Compatible Financial Goals

Traditional SMART goals fail ADHD professionals at the motivation layer. A goal that is specific, measurable, and time-bound but emotionally inert won't generate the sustained engagement the ADHD brain needs.

Financial goals that work here need emotional resonance — a connection to identity, values, or something that actually excites you. "Save $30,000 in 12 months" is a SMART goal. "Build enough runway to leave the job that's burning me out and launch my own practice" is a goal an ADHD brain can get behind.

Neural Revolution's DREAMS™ framework, developed by Dr. Eliza Barach, is built on this principle. Where SMART goals assume neurotypical motivation, DREAMS™ is designed around how ADHD motivation actually works — emotionally resonant, values-connected, and brain-aligned from the start.

Automate Everything: The ADHD Professional's Financial Infrastructure

The Core Principle

Every decision and action step you remove from financial maintenance is one fewer place for executive function to fail. Automation doesn't require willpower, working memory, or task initiation — or any initiation at all. It runs whether your executive function is running or not. Design your financial systems for your worst cognitive day, not your best.

What to Automate

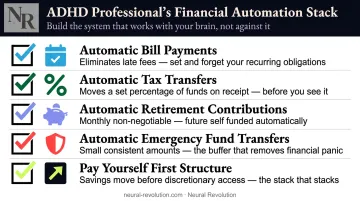

Every ADHD professional should have these in place:

- Automatic bill payments — eliminates late fees from the equation entirely

- Automatic tax transfers — a fixed percentage of every payment received moves immediately to a dedicated tax account (see the IRS Self-Employed Tax Center for calculating your specific obligation)

- Automatic retirement contributions — scheduled monthly, non-negotiable

- Automatic emergency fund transfers — even small amounts, consistently

- "Pay yourself first" structure — savings and tax transfers move before discretionary funds become accessible

Automatic Expense Categorization

Connecting bank and credit accounts to financial software removes one of the highest-friction behaviors for ADHD brains: manual transaction tracking. When expenses categorize themselves, the cognitive burden drops from "sustained, tedious data entry" to "quick review."

CHADD points to tools that send reminders, track bills, and reduce the working memory load of financial monitoring. YNAB (You Need A Budget) is built on zero-based budgeting logic that suits ADHD professionals — you're allocating money to jobs before spending it, which is clearer and more concrete than retroactive tracking.

The Review Cadence You Still Need

Automation is not "set and forget." Quarterly at minimum, ADHD professionals need a structured review to:

- Catch errors or unauthorized charges

- Adjust percentages for income changes

- Ensure automations still match current goals

The trick: pair this review with something already on the calendar — a quarterly business planning session, a tax check-in, anything with an existing date. Tethering it to an established event removes the need to initiate it from scratch.

Managing Variable Income and Irregular Cash Flow

Variable income is destabilizing for any professional, but it's particularly volatile for ADHD brains. High-income months trigger dopamine-driven spending and a sense of abundance. Lower-income months trigger avoidance and the impulse to not look at numbers at all. The result is a boom-and-bust cycle that keeps financially capable professionals perpetually behind.

Research confirms the pattern: ADHD symptoms are associated with both self-employment and unemployment — often in the same individual across different life periods. The same traits that drive entrepreneurial independence also create real financial vulnerability.

Pay Yourself a Salary

The single most stabilizing strategy for ADHD professionals with variable income: calculate your average monthly income over the prior 12 months and pay yourself that amount consistently, regardless of what came in that month. Excess pools in your business account as a buffer during lower months.

This eliminates month-to-month emotional volatility. Spending decisions no longer hinge on what happened to land in your account this week — you're operating from a stable, predictable number instead.

To make it work, the setup matters:

- Calculate your average monthly deposits over the past 12 months

- Set a recurring transfer on payday (same amount, same date each month)

- Let surplus accumulate in your business account as a low-month buffer

- Revisit the salary number every six months as income changes

Quarterly Tax Obligations

For ADHD entrepreneurs and freelancers, missed quarterly estimated tax payments are among the most common and costly financial failure points. The self-employment tax alone runs 15.3% (12.4% Social Security + 2.9% Medicare) — before federal and state income tax — and the IRS expects quarterly payments, not an annual lump sum.

The strategy that works: transfer a fixed percentage of every payment received directly to a dedicated tax account the day you receive it — automated if possible, always separate from operating funds. That account has one job. Don't reassign it.

Tools, Apps, and Getting the Right Support

Tools That Work for ADHD Brains

The criteria for ADHD-friendly financial tools: visual, simple, real-time feedback, minimal manual data entry.

| Tool Category | What It Does | Why It Works for ADHD |

|---|---|---|

| Zero-based budgeting apps (e.g., YNAB) | Allocates money to categories before spending | Concrete, decision-reducing, visual |

| Bank-syncing expense trackers | Auto-categorizes transactions | Removes manual data entry burden |

| Accounting software (e.g., QuickBooks, FreshBooks) | Tracks business income/expenses | Syncs invoicing with cash flow visibility |

| Bill reminder apps | Sends alerts before due dates | Compensates for working memory gaps |

The best tool is the one you'll actually open. Complexity is the enemy.

Tools only go so far, though. For many ADHD professionals, the bigger gap isn't finding the right app — it's having the right people in place.

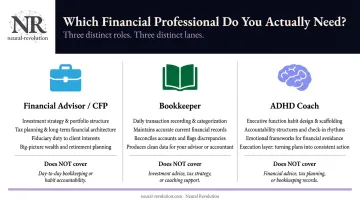

Understanding Which Professional You Actually Need

Most ADHD professionals have financial knowledge. What they're missing is the scaffolding to act on it consistently — and three different professionals cover three distinct layers of that:

- Financial advisor (CFP) — investment strategy, tax planning, long-term financial structure. Operates as a fiduciary in your best interest.

- Bookkeeper — transaction tracking, categorization, keeping your records accurate and current.

- ADHD coach — building the executive function habits, accountability structures, and emotional frameworks that make financial tools and plans stick.

The coach isn't doing your bookkeeping or managing your investments. They're addressing the layer underneath: why the invoices aren't getting sent, why the tax account never gets funded — and why you open YNAB for three weeks and then quietly stop.

For many ADHD professionals, coaching is the missing piece — not because they lack financial knowledge, but because knowledge without a system to execute it doesn't produce outcomes.

At Neural Revolution, coaching for solo consultants, entrepreneurs, and high-performing professionals focuses on:

- Billing and collections systems that survive ADHD admin avoidance

- Financial visibility patterns owners can actually sustain

- The procrastination and task initiation barriers that make financial administration fall apart

The approach is built around how your specific brain works — not a neurotypical productivity default.

Frequently Asked Questions

Do people with ADHD have problems managing money?

Yes. ADHD directly affects financial management through executive function deficits in working memory, impulse control, and planning. Research shows adults with ADHD report significantly more debt, less savings, and higher rates of impulse buying than neurotypical adults — even when financial knowledge is present.

Why is budgeting so hard for people with ADHD?

Budgeting requires sustained attention, future-focused thinking, and working memory — all areas impaired by ADHD. Most budgeting systems were designed for neurotypical brains and generate enough friction that ADHD brains quickly abandon them.

How can ADHD professionals stop impulse spending?

Three strategies work well together: enforce a 24–48 hour rule before any non-essential purchase; keep discretionary funds in a separate account with a fixed limit to cap exposure; and find high-interest activities that meet the brain's dopamine need without a price tag — working with the impulse rather than just against it.

What is the best budgeting method for an ADHD brain?

Simple, visual, and flexible wins every time. The buckets/jam jar method, zero-based budgeting apps like YNAB, or multiple labeled accounts all work well — because they're concrete and low-friction. The best method is whichever one is simple enough that you'll actually use it consistently next month.

Can an ADHD coach help with financial management?

An ADHD coach doesn't replace a financial advisor, but they address the execution layer — building the habits, accountability structures, and systems that make it possible to follow through on financial plans consistently. For many ADHD professionals, that execution layer is precisely what's been missing.